Last Update: Tue, Jul 21, 2026 5:43 AM

Total Views: 35022

Corporate taxation is one of the essential financial obligations businesses must adhere to when operating in Egypt. Whether a multinational corporation, a small local enterprise, or a foreign branch, understanding corporate tax laws is vital for staying compliant with legal requirements. In this post, we will explore the fundamentals of corporate tax in Egypt, including who needs to pay it, applicable tax rates, deductions, filing requirements, and common mistakes to avoid.

What is Corporate Tax in Egypt?

Corporate tax is a levy imposed on the profits of companies that operate within a country’s borders. In Egypt, all companies that generate income, whether Egyptian-owned or foreign branches, are subject to corporate taxation. The Egyptian tax system requires businesses, whether large enterprises or small local firms, to pay taxes on their annual profits. The system also applies to foreign companies with branches or operations in Egypt, ensuring that all businesses contributing to the local economy are held accountable for their tax obligations.

Corporate tax is crucial for supporting the government’s ability to fund public services and infrastructure projects, making it a central component of Egypt’s broader economic structure.

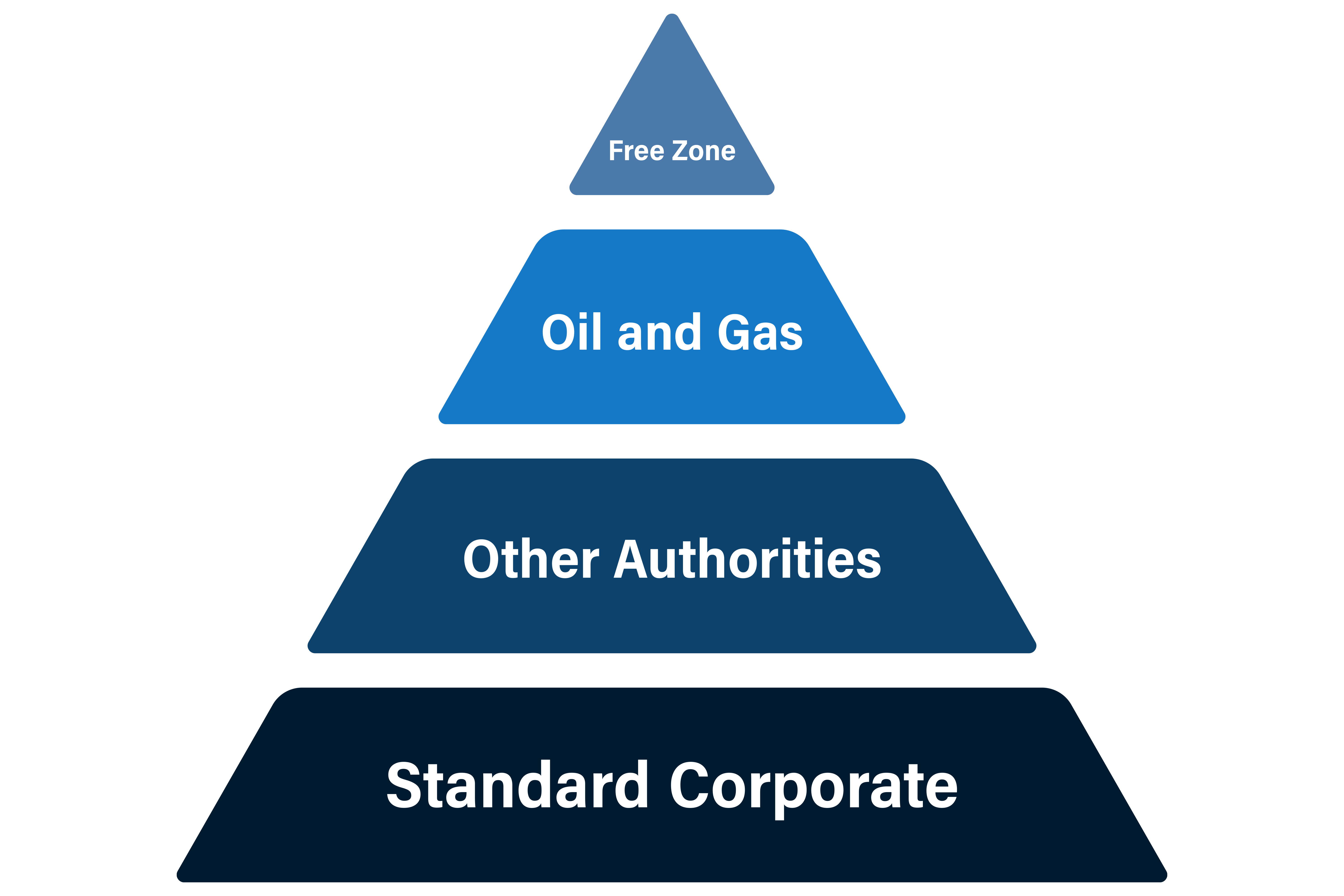

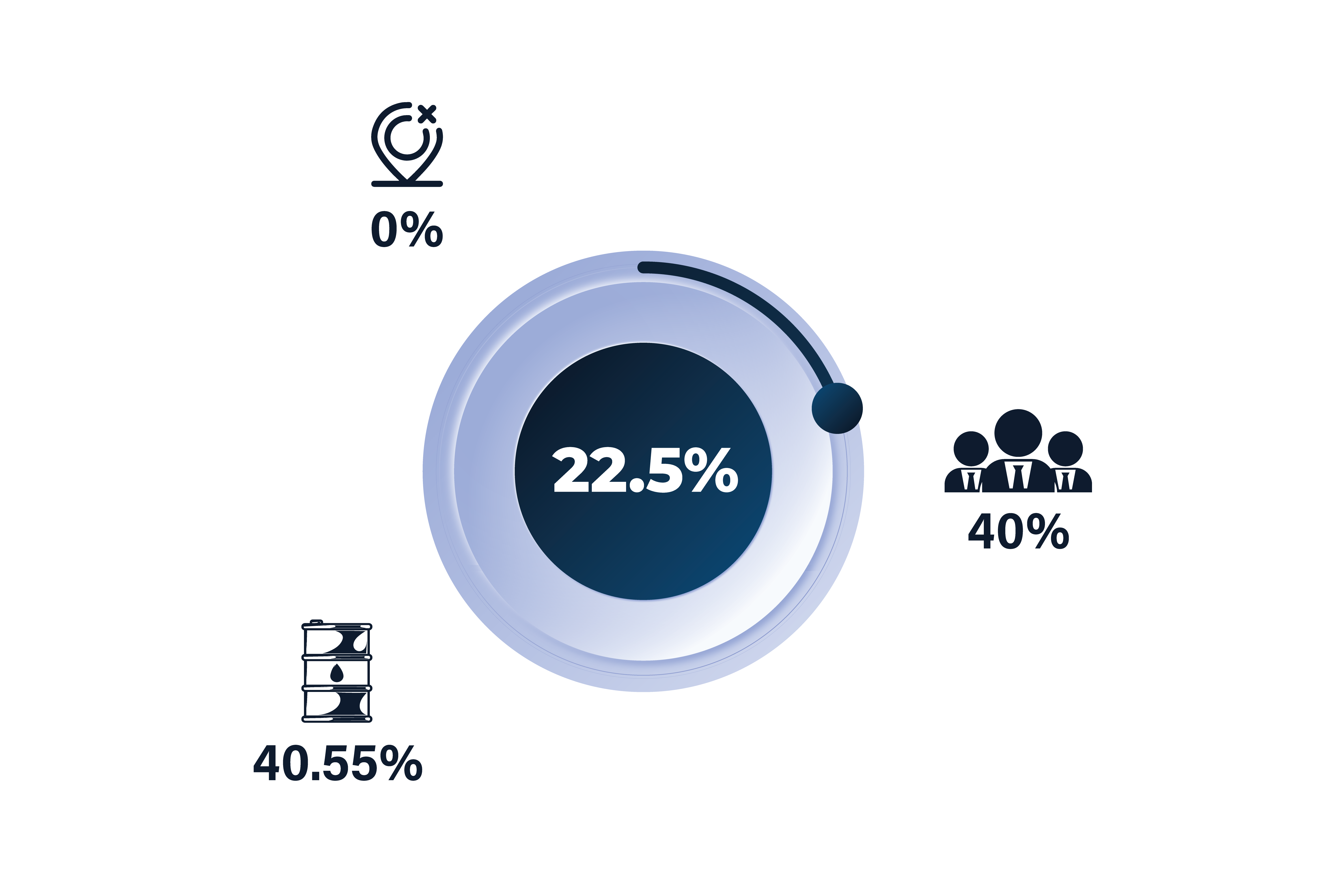

Corporate Tax Rates in Egypt

The general corporate tax rate in Egypt currently stands at 22.5%, making it one of the region’s competitive rates for businesses. However, there are specific sectors where tax rates may differ. For instance, the oil and gas industry, which has long been a cornerstone of Egypt’s economy, is subject to higher tax rates, with some companies facing rates of up to 40%. Similarly, businesses involved in exploration and production may also encounter different taxation structures.

Despite these variations, the flat 22.5% rate applies to most businesses, regardless of their size or the industry they operate in. This stability helps make Egypt an attractive market for foreign investment and local entrepreneurship alike.

Corporate Tax Deductions and Allowances

Egypt’s tax system allows for a range of deductions and allowances that can help reduce a company’s overall tax liability. Some of the most common deductions include:

- Depreciation of Assets: Companies can deduct the depreciation of their capital assets, such as machinery, equipment, and buildings. This helps businesses recover part of the costs associated with large investments over time.

- Loss Carryforward: If a company experiences losses in a particular tax year, those losses can be carried forward and deducted from future profits, up to a certain limit. This is especially beneficial for startups and businesses in volatile industries.

- Investment Incentives: Egypt offers tax incentives for businesses that invest in certain sectors or regions, such as free zones or new urban communities. These incentives may include tax holidays or reduced tax rates for a specified period, encouraging investment in key areas of economic development.

- Charitable Contributions: Businesses can also deduct donations made to charitable organizations, provided they meet certain criteria.

Understanding and effectively utilizing these deductions is crucial for optimizing your company’s tax strategy and ensuring compliance with Egyptian tax laws.

Corporate Tax Filing Requirements

Corporate tax returns in Egypt must be filed annually, with the deadline typically set at the end of April following the tax year. Companies must submit their tax returns electronically, along with all necessary documentation to substantiate their reported income, expenses, and deductions. Required documents may include financial statements, proof of income, and records of any deductions claimed.

Failure to file taxes on time or provide accurate documentation can result in penalties, which may include fines or increased scrutiny from tax authorities. It’s critical for businesses to stay ahead of filing deadlines and ensure that all financial records are properly maintained throughout the year.

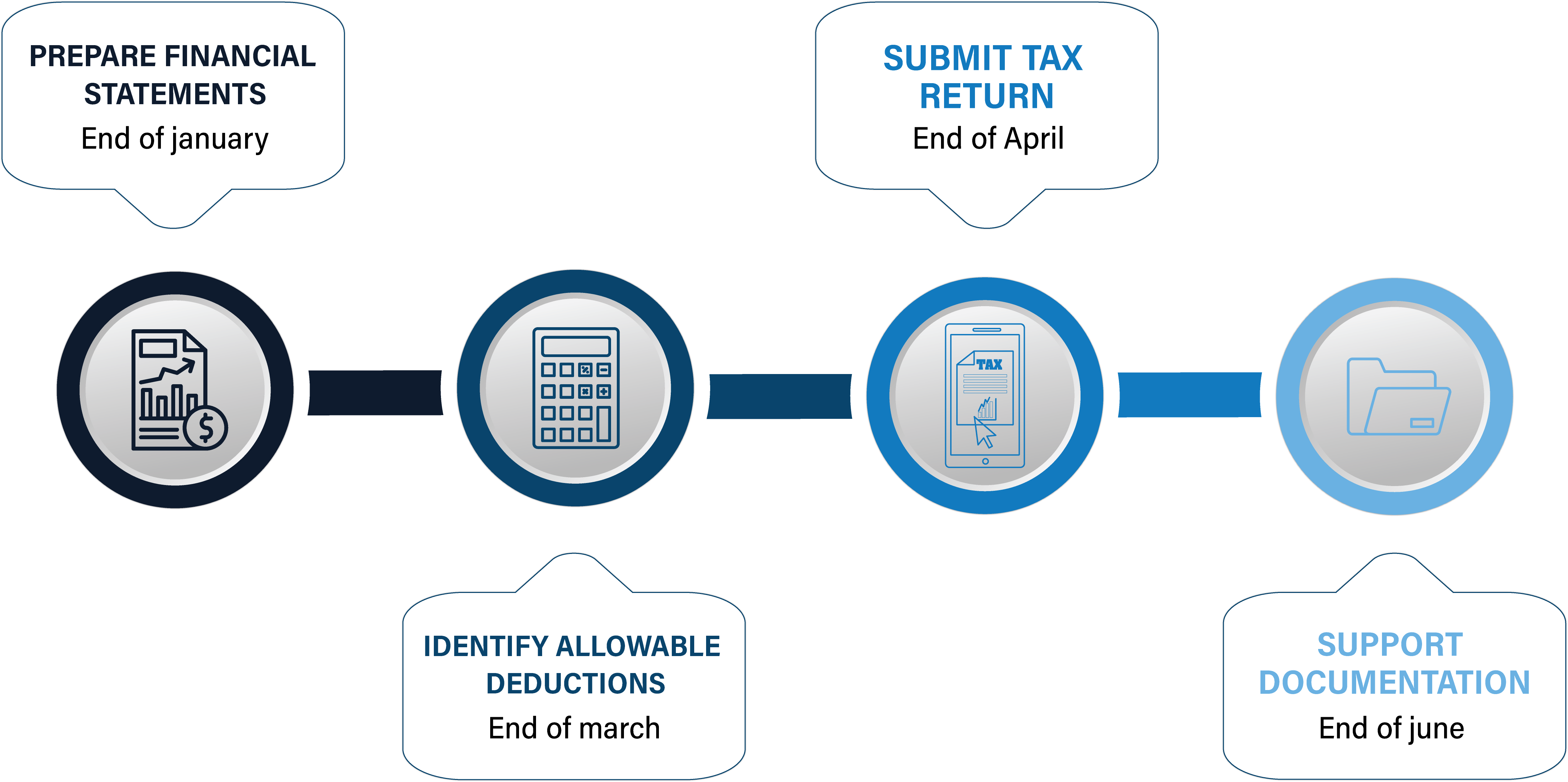

Here’s a quick look at the corporate tax filing process:

- Prepare financial statements for the tax year, including profit and loss statements, balance sheets, and cash flow statements.

- Identify allowable deductions and apply them to reduce your taxable income.

- Submit your tax return electronically through the Egyptian Tax Authority’s platform.

- Ensure all documentation is ready to support your claims, including invoices, receipts, and financial reports.

Common Corporate Tax Mistakes to Avoid

Even the most experienced businesses can make errors when filing their corporate taxes. Here are some of the most common mistakes and how to avoid them:

- Missing Deduction Opportunities: Businesses often fail to take full advantage of available deductions, such as depreciation or loss carryforwards. Make sure your finance team is well-versed in all the deductions you qualify for.

- Inaccurate Documentation: Failing to provide the correct documentation to support your claims is a major pitfall. Always keep meticulous records of all income, expenses, and deductions to avoid any discrepancies.

- Late Filing: Missing the corporate tax filing deadline can result in hefty fines and penalties. Be sure to prepare your tax return well ahead of the April deadline to avoid any last-minute issues

- Not Staying Up-to-Date on Tax Laws: Tax regulations can change from year to year. Make it a point to stay informed about any new tax laws or reforms that might affect your business operations.

By avoiding these common pitfalls, businesses can ensure they remain in good standing with the Egyptian Tax Authority and minimize their tax liability effectively.

Conclusion

Corporate taxation in Egypt is a key component of doing business in the country, and understanding its fundamentals is critical for every company, big or small. By staying informed about the corporate tax rate, making use of available deductions, and adhering to proper filing requirements, businesses can ensure they remain compliant with the law while optimizing their tax strategy.

While taxes can often be a complex and intimidating aspect of running a business, proper planning and awareness of tax regulations can go a long way in ensuring smooth financial operations. Keep your records accurate, stay updated on tax laws, and approach the filing process methodically to avoid potential pitfalls.